Conveyancing, real estate

We break down all you need to know about GST WITHHOLDING when buying or selling a property in Queensland...

Prefer to watch/listen? Click here to consume this content via YouTube!

GST Withholding

Ok, so since the above questions appeared on page 4 of the July 2018 REIQ Contracts, most professionals have not taken the time to understand what they mean and why they were implemented.

Well, we have finally decided to take a deeper dive into GST Withholding in QLD contracts and explain all you need to know.

The purpose of the GST Withholding is to oblige the GST that is owing on a property contract dated from 01 July 2018 is collected and paid directly to the ATO, as a part of the settlement process.

Please note that the GST withholding is not an additional amount on top of the purchase price - instead it comes out of the sale proceeds and is paid by the Vendor.

Who is eligible?

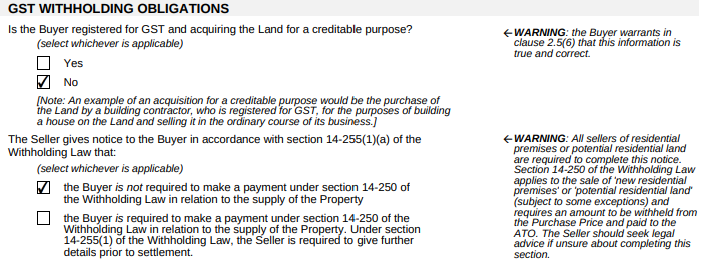

The sale of residential (or potential residential) land that involves subdivision or new residential land (i.e developments) will likely require GST withholding.

There is significant confusion surrounding whether a property is eligible for GST withholding. The GST withholding requirement is only applicable when the sale of residential land is a taxable supply for GST purposes.

The supply of subdivided residential land is a taxable supply when the supply is made via an enterprise - for example property developers, or by an entity that is registered (or required to be registered) for GST.

Your typical "mum & dad" purchase or sale will likely not attract GST withholding obligations. If you are unsure, we suggest you speak with your accountant.

Why GST withholding?

GST withholding laws changed in 2018 to stop "phoenixing". Phoenixing is the process whereby a company that sells properties as their business (i.e a developer) winds up their business prior to paying the GST owning. By shifting the burden to the Purchaser to collect the GST owing - the ATO gets paid and the revenue is not lost.

Vendor Responsibilties:

The Vendor must give the Purchaser written notice, prior to settlement, outlining (amongst other things), the amount that is to be withheld. This information is sent to the Purchaser's Solicitors - so they can arrange for the payment to be made as part of the settlement process.

Usually, this amount is 1/11th of the contract purchase price, or 7% if the Margin Scheme applies. The Vendor will obtain the correct formula and amounts from their accountant.

Failure to comply will attract a maximum penalty of $21,000 for individuals, and $105,000 for companies.

Purchaser Responsibilties:

The Purchaser must notify the Commissioner of the amout that is to be withheld (Form 1). This occurs prior to settlement. Form 2 is required at the time of payment of the GST withholding. This process is organised by the Purchaser's Solicitors.

The Purchaser must also advise if they are registered for GST, and acquiring the property for a creditable purpose (to conduct business). An example of a creditable purpose would be a builder purchasing land from a developer to build and resell.

Penalty: A Purchaser who fails to withhold or provide a bank cheque made payable to the Commissioner is liable for an administrative penalty equal to the amount that should have been withheld plus interest .

Hopefully this short blog helped to explain what GST withholding is, when it applies and how to deal with it. The lesson to take away is....if you are unsure, get the vendor/purchaser to ask their accountant!

We can help…

For simple, sunny, smooth sailing conveyancing - Empire Legal.

We look forward to continuing to help thousands of Queenslanders every year with their conveyancing!

Any questions? Want to know more? Get in contact with us via the below form or via info@empirelegal.com.au.

Note: all information is general in nature and as each matter is unique please contact our office for tailored advices: the above does not constitute legal advice.